South Carolina is sitting on a gold mine it refuses to touch. While neighboring states quietly rake in hundreds of millions from legalized online gambling, the Palmetto State remains one of the strictest anti-gambling jurisdictions in the entire United States – no lottery, no casinos, no regulated sports betting. But a sweeping new market research report has put hard numbers behind what analysts have long suspected: the suppressed demand here is enormous, the political winds are slowly shifting, and the operators paying attention right now will be the ones who own the market when the dam finally breaks.

- South Carolina’s potential iGaming market is estimated at $1.4 billion annually, driven by pent-up demand from an unserved adult population of over 4 million.

- The state currently has a near-total gambling prohibition, making it one of only a handful of holdouts in the Southeast.

- Player migration to offshore and neighboring-state platforms is already significant, meaning revenue is flowing out of South Carolina right now.

- Legislative momentum is building, with recent sessions seeing the first serious iGaming and sports betting bill discussions in over a decade.

- Tax revenue modeling suggests the state could fund education and infrastructure at levels comparable to New Jersey’s early iGaming windfall years.

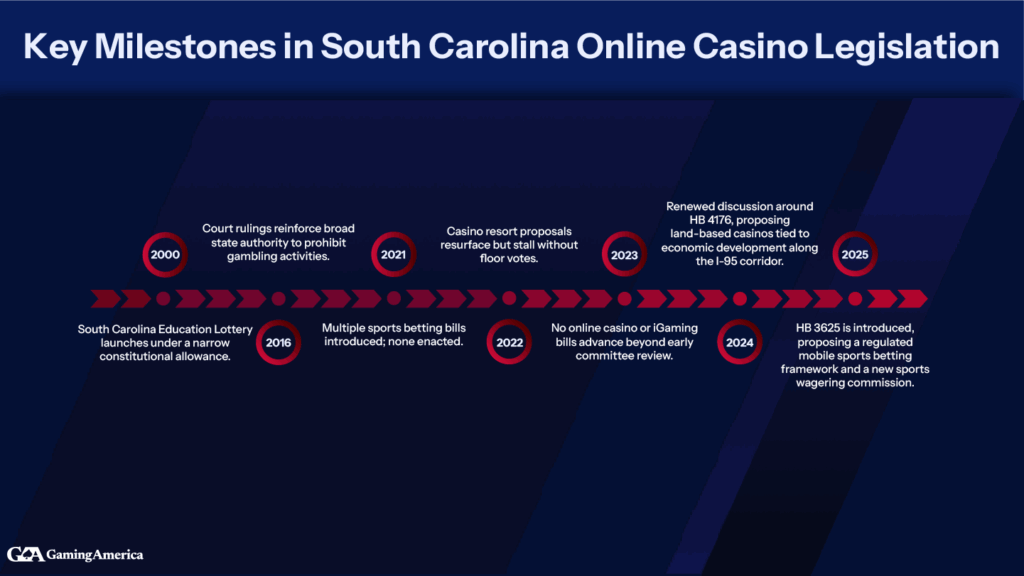

The Lay of the Land: A Prohibition-Era State in a Post-PASPA World

To understand the South Carolina iGaming opportunity, you need to understand just how uniquely restrictive its legal framework is. The state constitution explicitly prohibits lotteries, and decades of evangelical political influence have kept any form of commercial gambling firmly off the table. This is not a market that missed the wave – it actively built a seawall against it.

The 2018 Supreme Court ruling in Murphy v. NCAA – the decision that dismantled the federal sports betting monopoly – cracked that seawall. Since then, 38 states have moved to legalize sports wagering in some form. South Carolina has not. But the research report makes a compelling case that the conversation is no longer if, but when. And when it comes to iGaming specifically, the state’s geographic and demographic profile makes it one of the most compelling untapped markets in North America.

Analyst’s Note: The historical pattern across newly legalized states is consistent – operators and platforms that establish brand equity before the regulatory green light capture disproportionate market share at launch. South Carolina’s prolonged prohibition creates an unusually long runway for pre-market positioning.

Breaking Down the $1.4 Billion Revenue Projection

The headline number deserves scrutiny. How does a state with zero legal gambling infrastructure arrive at a $1.4 billion annual iGaming revenue estimate? The methodology combines three core inputs that any serious analyst would recognize as the industry standard framework.

Adult Population and Participation Rates

South Carolina has approximately 4.1 million adults. The report applies a participation rate of 18-22% for online casino games and 14-17% for online sports betting – figures derived from comparable markets in Pennsylvania and Michigan during their first two years of operation. Apply those percentages to 4.1 million people and you get an active player pool in the range of 580,000 to 900,000 individuals. That is the foundation.

Average Revenue Per User (ARPU) Modeling

The report uses a blended ARPU figure of approximately $1,550 annually, segmented across casual players, regular players, and high-value players. This is deliberately conservative. Pennsylvania’s iGaming ARPU has consistently run above $1,800. The discount accounts for South Carolina’s lower median household income relative to the national average and the expected initial novelty spike followed by market stabilization.

Player Migration and Leakage Recovery

This is the data point that should alarm state legislators. A meaningful percentage of South Carolina residents are already gambling online – on offshore platforms operating in legal gray zones, or by physically crossing into Georgia, North Carolina (which has limited tribal gaming), or traveling to Atlantic City and Las Vegas. The report estimates that between $180 million and $240 million in annual gambling spend is currently leaving South Carolina’s economy entirely, generating zero state tax revenue and zero consumer protection. Legalization does not create this spending – it captures it.

Pro Tip: When evaluating state iGaming market projections, always separate “new” gambling spend from “recovered” offshore spend. South Carolina’s high leakage rate actually de-risks the revenue projection – a significant portion of that $1.4B already exists, it just flows offshore.

The Regulatory Landscape: Reading the Political Tea Leaves

South Carolina’s legislature operates with a Republican supermajority that has historically treated any gambling expansion as a non-starter. That calculus is changing, and the research report documents the shift with precision.

Recent Legislative Activity

The 2023-2024 session saw House Bill 3749 introduced – the first substantive sports betting legalization proposal to receive committee discussion in over a decade. The bill did not advance, but its introduction signals that the Overton window is moving. Key sponsors included representatives from coastal districts like Myrtle Beach and Hilton Head, where tourism economies create natural alignment with entertainment-adjacent industries.

The Education Funding Angle

Every state that has successfully legalized iGaming has used a specific political wedge: education funding. South Carolina ranks in the bottom quartile of states for per-pupil education spending. The report models a tax rate scenario at 15% of gross gaming revenue – the median among regulated states – which would generate an estimated $210 million annually for state coffers. That number is politically potent when framed as teacher salaries and school infrastructure rather than casino profits.

Tribal and Commercial Operator Dynamics

Unlike some Southern states, South Carolina has no established tribal gaming compact, which eliminates one traditional lobbying obstacle to commercial iGaming. The Catawba Nation, however, completed a Kings Mountain casino development in North Carolina just across the border – a project that has put Native American gaming interests back into the regional political conversation. How that dynamic plays into a South Carolina licensing framework, if one emerges, remains a key variable.

Competitive Positioning: Who Wins If the Market Opens

The report’s operator analysis is where the industry pulse gets genuinely interesting. Assuming a legalization timeline of 2026-2028 – which the report tags as its base case scenario – the competitive landscape would likely feature a limited-license model similar to what Michigan deployed at launch.

DraftKings, FanDuel, and BetMGM have the national brand recognition and capitalization to dominate early market entry. But the report flags a counterintuitive finding: states with longer prohibition periods tend to show stronger performance for regional and mid-tier operators in years two through four, as local brand affinity and targeted marketing outperform national spray-and-pray acquisition strategies.

The customer acquisition cost (CAC) environment in a newly opened South Carolina would be competitive but not ruinous by industry standards. The offshore player segment – estimated at 8-12% of the adult gambling population – represents a high-value, high-intent cohort that is already educated on iGaming products and requires minimal conversion spend. These are not players who need to be convinced that online gambling is appealing. They need a legal, trusted platform to migrate to.

Infrastructure and Technology Readiness

A frequently overlooked dimension of market readiness is the technical and regulatory infrastructure required to support a legal iGaming market. South Carolina would need to establish a Gaming Control Board or equivalent regulatory body, implement geofencing and geolocation compliance technology, build a problem gambling support infrastructure, and negotiate tax collection frameworks – all before a single legal bet could be placed.

The report estimates a 12-18 month regulatory buildout timeline from legislation passage to first legal wager, which is consistent with the national average. Pennsylvania took 14 months. Michigan took 16. There is no shortcut here, and operators who underestimate the compliance complexity in a new market consistently underperform at launch.

The Bottom Line

South Carolina’s iGaming market is not a question of demand – that case has been made definitively. It is not even a serious question of economic benefit – the revenue modeling is conservative and credible. The only real question is political timing, and the evidence suggests the window is narrowing. For operators, investors, and platform providers, the strategic calculus is straightforward: the time to build relationships, understand the regulatory terrain, and establish early positioning is before the legislation passes, not after. The states that figured that out early are the ones writing the largest checks to state governments today.