Oregon has never been the loudest voice in the American gambling conversation. Nevada gets the glamour, New Jersey gets the credit for online pioneer status, and Pennsylvania gets the volume. But a closer look at the latest iGaming market research report on Oregon reveals something the mainstream narrative keeps glossing over: this Pacific Northwest state is sitting on a quietly enormous, structurally sound, and politically complex iGaming opportunity that operators and investors can no longer afford to ignore.

The Oregon iGaming market is not a blank canvas. It has an existing lottery infrastructure, tribal gaming compacts, and a digitally engaged consumer base that is already spending money online. The question is not whether online gambling will arrive in Oregon. The question is who controls it, how fast it scales, and what the regulatory architecture will look like when it does.

- Oregon’s iGaming market is underpinned by an established state lottery and tribal gaming ecosystem, giving it a structural head start over greenfield markets.

- The state’s digitally active adult population represents a high-value player pool that is already engaging with unregulated offshore platforms.

- Tribal sovereignty and compact negotiations remain the single biggest variable in any Oregon online gambling expansion timeline.

- Revenue projections position Oregon as a mid-to-large iGaming market by U.S. standards, comparable to states like Michigan in its early regulatory phase.

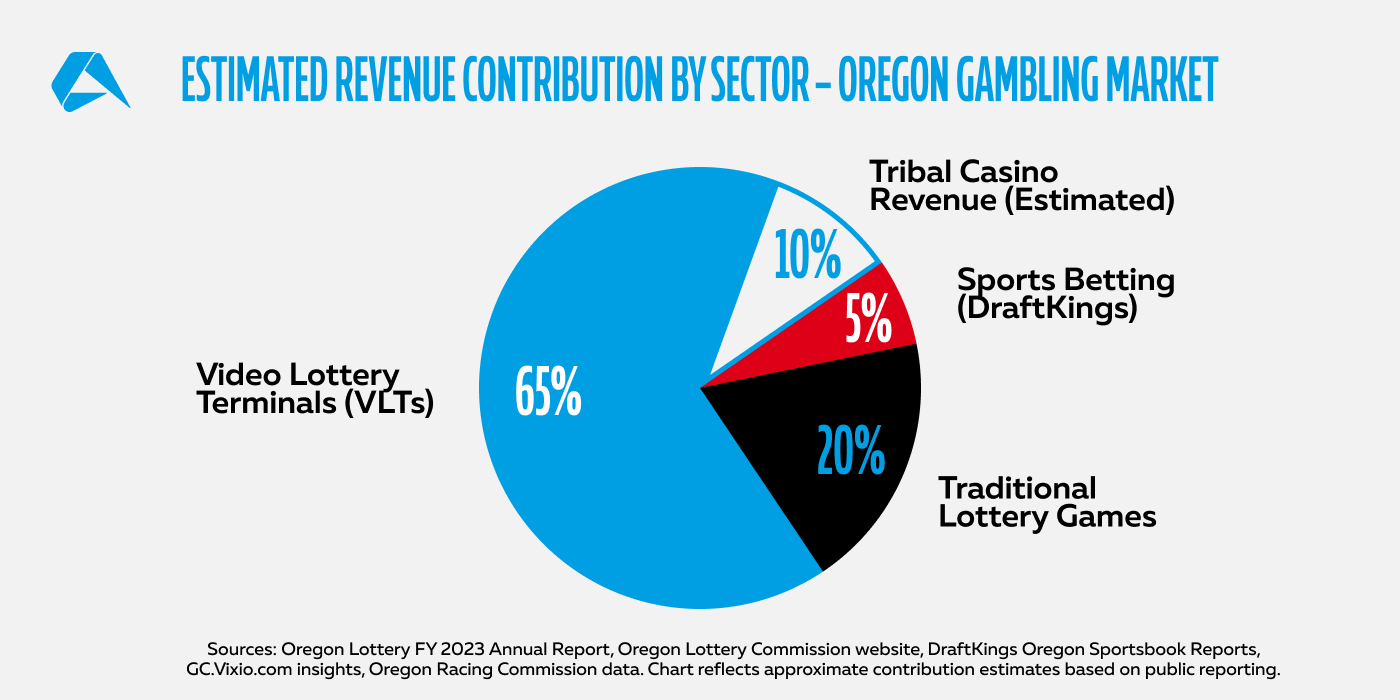

- Sports betting, already live via the Oregon Lottery’s

Scoreboardapp, is the beachhead product that signals broader digital gambling appetite.

The Market Architecture Oregon Already Has

Before any analyst projects forward, you have to account for what Oregon has already built. The Oregon Lottery is not a passive institution. It operates iLottery products, manages the Scoreboard sports betting application, and has demonstrated a clear willingness to compete in digital channels. That is a meaningful distinction from states where lottery commissions are purely brick-and-mortar operations resisting digital transition.

The Scoreboard app launched in 2019 and gave Oregon one of the earliest state-operated mobile sports betting products in the country. It is clunky by commercial operator standards, and the odds have historically been less competitive than what DraftKings or FanDuel offer, but it proved two things: Oregon consumers will bet online, and the state is not philosophically opposed to digital wagering infrastructure.

Tribal Gaming’s Central Role

Any serious Oregon iGaming analysis has to wrestle with the tribal dimension. Oregon is home to nine federally recognized tribes, and tribal gaming compacts govern a substantial portion of casino-style gambling in the state. The Confederated Tribes of Warm Springs, the Cow Creek Band of Umpqua Tribe of Indians, and others operate facilities that would be directly affected by any iGaming expansion framework.

This is not a hostile dynamic by default. Several U.S. states, Michigan being the clearest model, have successfully negotiated iGaming frameworks that give tribal operators a meaningful seat at the digital table. Oregon’s tribes have shown political sophistication in compact negotiations historically, and the more likely outcome is a hybrid model where both the state lottery and tribal-affiliated platforms participate, rather than a winner-take-all structure.

Analyst’s Note: The Michigan model, where tribal and commercial operators coexist under a unified regulatory framework, is the most probable template for Oregon. States that tried to exclude tribal operators from digital expansion faced years of litigation and delayed revenue capture. Oregon’s political leadership has strong incentives to avoid that outcome.

The Revenue Opportunity in Hard Numbers

Market sizing for Oregon iGaming depends heavily on regulatory scope. A lottery-only online casino model captures the smallest share. A fully licensed commercial and tribal iGaming market, inclusive of online slots, table games, and poker, opens the ceiling considerably.

Oregon’s adult population sits at approximately 3.3 million. Consumer research on iGaming adoption rates in comparable regulated states suggests a realistic active player penetration of 4 to 7 percent in a mature market. At an average gross gaming revenue per active player of roughly $600 to $800 annually, a fully operational Oregon iGaming market could generate between $79 million and $185 million in annual GGR at maturity, with tax revenue to the state likely falling in the $20M to $55M range depending on the tax rate structure negotiated.

Those numbers are not Michigan-scale, but they are not trivial either. For context, Delaware’s iGaming market, one of the smallest regulated markets in the U.S., generates approximately $50 million annually. Oregon’s superior population base and higher median household income profile suggest it would outperform Delaware substantially within two to three years of launch.

Sports Betting as the Revenue Bridge

The existing Scoreboard infrastructure is underperforming against its potential, primarily because the Oregon Lottery operates it as a monopoly without the marketing budgets, odds competitiveness, or product depth that commercial operators bring. Legislative pressure to either modernize the lottery’s offering or open the market to licensed commercial sportsbooks is building.

A competitive sports betting market in Oregon, modeled after New York’s approach of high-tax licensed commercial operators, could generate $30M to $60M in annual state tax revenue alone. That figure, once demonstrated, historically accelerates the political appetite for broader iGaming expansion, which carries higher margins and more consistent revenue than sports betting’s inherently volatile hold percentages.

Regulatory Risk Factors and Timeline Realities

The optimistic scenario projects a regulated Oregon iGaming market within three to five years. The pessimistic scenario involves a decade of compact renegotiation, legislative gridlock, and continued lottery monopoly entrenchment. The realistic scenario sits closer to the middle.

Key Legislative Variables

Oregon’s legislature operates in biennial sessions, which compresses the windows for major policy movement. Any iGaming bill would need to navigate the Senate Judiciary Committee, address tribal consultation requirements under federal law, and survive a governor’s signature process under an administration that has historically prioritized public health framing around gambling expansion.

The offshore leakage problem is arguably the strongest argument for acceleration. Oregon residents are already spending an estimated $150M to $300M annually on unregulated offshore casino sites. That revenue currently generates zero state tax receipts, zero consumer protection oversight, and zero economic benefit to Oregon-based operators or tribes. Framing iGaming legalization as revenue recapture rather than gambling expansion has proven effective in other states and is likely the messaging strategy advocacy groups will deploy in Salem.

Pro Tip: Operators eyeing Oregon market entry should prioritize tribal partnership outreach now, before legislative frameworks are set. The operators who secured Michigan tribal partnerships early locked in favorable revenue-sharing terms that late entrants could not replicate. Oregon will follow the same first-mover dynamic.

Competitive Landscape and Operator Strategy

If and when Oregon opens, the competitive environment will be immediate and intense. DraftKings, FanDuel, BetMGM, and Caesars have proven they will enter any state with a viable addressable market, and Oregon qualifies. However, the state’s tribal gaming infrastructure means that local-first operators with established compact relationships could have a meaningful distribution advantage in the early launch window.

Platform providers should note that Oregon’s consumer tech sophistication is high. Portland and the broader Willamette Valley corridor have concentrated tech-sector demographics that correlate strongly with higher average player values, lower friction in digital onboarding, and stronger retention rates for app-based products. The product quality bar for market entry will need to be elevated accordingly.

The Bottom Line

Oregon’s iGaming market report tells the story of a state that is further along the readiness curve than its current regulatory status suggests. The infrastructure exists. The consumer demand is demonstrably present. The revenue case is numerically sound. What remains is the political will to negotiate a framework that honors tribal sovereignty, captures offshore leakage, and builds a competitive market that benefits Oregon residents rather than offshore operators.

The states that moved decisively on iGaming in the 2020 to 2022 window are now reporting nine-figure annual revenues. Oregon is watching that happen from the sideline. The research suggests the sideline phase is nearing its end.