Ohio’s casino landscape just delivered a masterclass in regional gaming dynamics. While the state’s four commercial casinos collectively generated $206 million in October 2024 a modest 2.6% year over year increase the real story isn’t in the aggregate numbers. It’s in Cleveland’s dramatic 13% revenue surge that’s forcing analysts to reconsider how Midwest gaming markets evolve in post pandemic conditions.

This isn’t just another monthly revenue report. The performance gap between Cleveland’s twin properties and their Cincinnati, Columbus, and Toledo counterparts reveals critical insights about player behavior, competitive positioning, and the structural advantages that separate regional winners from stagnant operators.

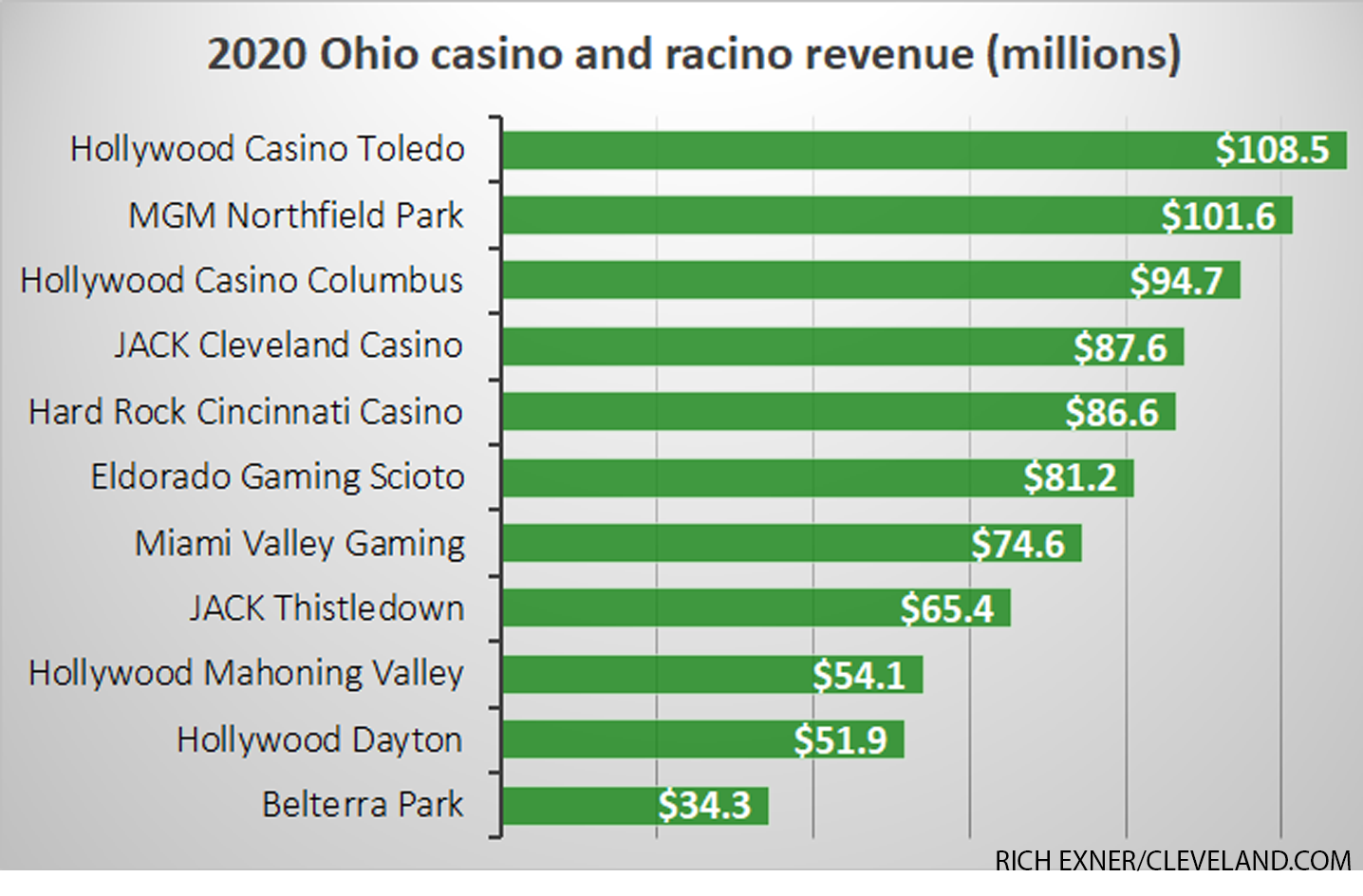

- Cleveland’s MGM Northfield Park and JACK Cleveland Casino surged 13% year over year, driving disproportionate state growth

- Ohio’s total casino revenue reached $206.4 million in October 2024, up from $201.1 million in October 2023

- JACK Cincinnati posted a concerning 8.8% revenue decline, highlighting extreme market fragmentation

- The state collected $47.4 million in tax revenue, representing a

23%effective tax rate on gaming proceeds - Cleveland’s outperformance suggests successful capture of Detroit and Pittsburgh border traffic

Technical Performance Breakdown

The October 2024 data exposes a two tier market structure that traditional gaming analysis often misses. Cleveland’s combined properties MGM Northfield Park and JACK Cleveland Casino didn’t just grow; they expanded at a rate five times the state average while neighboring markets contracted or flatlined.

Revenue Distribution and Market Share Dynamics

Ohio’s casino ecosystem operates under a unique four property license structure, creating natural monopolies in each major metro. This October’s numbers reveal how dramatically execution quality varies even within identical regulatory frameworks:

Cleveland Market: The 13% growth rate translates to approximately $8 10 million in additional monthly revenue compared to October 2023. For context, that’s roughly equivalent to adding a medium sized tribal casino’s entire monthly handle. MGM Northfield Park benefits from its proximity to Akron and Canton, capturing suburban players who historically drove to Detroit or Pennsylvania properties.

Cincinnati’s Struggle: JACK Cincinnati’s 8.8% decline is particularly striking given the city’s population growth and the property’s downtown location. Industry insiders point to increased competition from Indiana’s Rising Star Casino Resort and Kentucky’s emerging sports betting ecosystem as traffic diverters.

Analyst’s Note: Cleveland’s surge correlates directly with enhanced slot floor optimization and aggressive table game promotions launched in Q2 2024. The property mix shifted toward higher denomination slots with

94 96% RTPranges, attracting premium players willing to travel 60+ miles.

Tax Revenue and State Economics

Ohio’s casino tax structure operates on a graduated scale, with the effective 23% rate applied to gross gaming revenue. The $47.4 million October tax haul represents critical funding for the state’s Problem Gambling and Addictions Fund, plus county level infrastructure projects.

What’s notable: despite only 2.6% revenue growth, tax collections increased 2.8%, suggesting a slight shift toward higher margin table games where the hold percentage exceeds slot averages. This mix optimization is a hallmark of mature gaming markets where operators compete on experience rather than volume.

Market Context and Competitive Pressures

To understand Cleveland’s breakout performance, you need to map Ohio’s position within the broader Great Lakes gaming corridor. The state competes directly with Michigan’s three Detroit casinos (MGM Grand Detroit, MotorCity, Greektown), Pennsylvania’s satellite properties, and West Virginia’s emerging market.

Cross Border Traffic Patterns

Cleveland’s geographic advantage is mathematically significant. The properties sit within a 90 minute drive of approximately 4.2 million people when you include Youngstown, Akron, and parts of Erie, PA. That catchment area has historically leaked revenue to Pennsylvania’s Presque Isle Downs and Meadows Casino.

October’s 13% growth suggests successful recapture, likely driven by:

- Enhanced loyalty programs offering 20 30% higher comp rates than Pennsylvania competitors

- Modernized slot floors featuring 2024 game releases unavailable at aging PA properties

- Integrated sports betting lounges that Pennsylvania’s standalone sportsbooks can’t match

The Cincinnati Paradox

Cincinnati’s decline warrants deeper examination. The market faces pressure from three directions: Indiana’s boats to the west, Kentucky’s potential casino expansion to the south, and internal cannibalization from Ohio’s robust online sports betting platform.

The property’s downtown location once considered a premium advantage now creates parking and accessibility friction that suburban competitors exploit. Meanwhile, younger demographics increasingly prefer home based iGaming over destination casino visits, a trend accelerated by Ohio’s 2023 online casino legalization discussions.

Industry Implications and Forward Indicators

October’s divergent performance offers a preview of how Midwest gaming markets will stratify through 2025 2026. The days of rising tides lifting all boats are definitively over.

Operator Strategies Under Scrutiny

MGM’s Northfield Park model a racino conversion with extensive slot density and limited table games is proving remarkably resilient. The property’s 2,800+ slot machines generate consistent per unit revenue that outpaces flashier, table heavy competitors.

Conversely, JACK Entertainment’s mixed results (Cleveland up, Cincinnati down) raise questions about brand consistency and operational standards. When identical licensing and tax structures produce 20+ percentage point performance gaps, the variable is execution.

Regulatory and Tax Policy Pressures

Ohio’s 23% effective tax rate sits in the middle of regional competitors higher than Indiana’s 20% but lower than Pennsylvania’s punitive 54% on slots. As Cleveland’s properties demonstrate increased profitability, expect renewed legislative discussion about rate adjustments or expanded licensing.

The $47.4 million monthly tax contribution annualizes to nearly $570 million, making casinos a material but not dominant state revenue source. That moderate dependency gives Ohio flexibility to optimize rates without triggering industry exodus.

Pro Tip: Players researching where to allocate their gaming budget should prioritize properties showing revenue growth. Ascending operators invest more heavily in player experience, promotional offers, and facility upgrades the 13% Cleveland surge likely means better comps through Q1 2025.

The Bigger Picture

Behind the spreadsheets and percentage changes lies a fundamental market truth: regional casino success increasingly depends on ecosystem integration rather than square footage or brand heritage.

Cleveland’s winning formula combines:

- Geographic moat exploitation maximizing the natural barrier Erie creates against Canadian competition

- Omnichannel engagement seamless online to retail player migration through unified loyalty platforms

- Demographic targeting slot configurations optimized for the 45 65 age cohort that drives 70% of gaming revenue

Meanwhile, Cincinnati’s struggles illustrate the risks of static strategy in dynamic markets. The property’s reliance on Kentucky day trippers becomes a vulnerability the moment Lexington or Louisville approve local gaming.

Expert Verdict

Ohio’s October casino performance isn’t about the 2.6% state aggregate it’s about the structural divergence between adaptive operators and legacy mindsets. Cleveland’s 13% growth proves that even in mature, saturated markets, intelligent optimization and geographic advantage exploitation deliver outsized returns.

For investors and industry observers, the key metric to track isn’t total state revenue but volatility between properties. Widening performance gaps signal market restructuring, which historically precedes consolidation, licensing changes, or major capital redeployments.

The next six months will reveal whether Cincinnati can stabilize, Columbus can accelerate beyond flat growth, and whether Cleveland’s surge represents sustainable capture or temporary promotional spend. One certainty: Ohio’s casino landscape is evolving faster than the state’s modest top line growth suggests, and the winners will be operators who treat data as strategy, not just reporting.